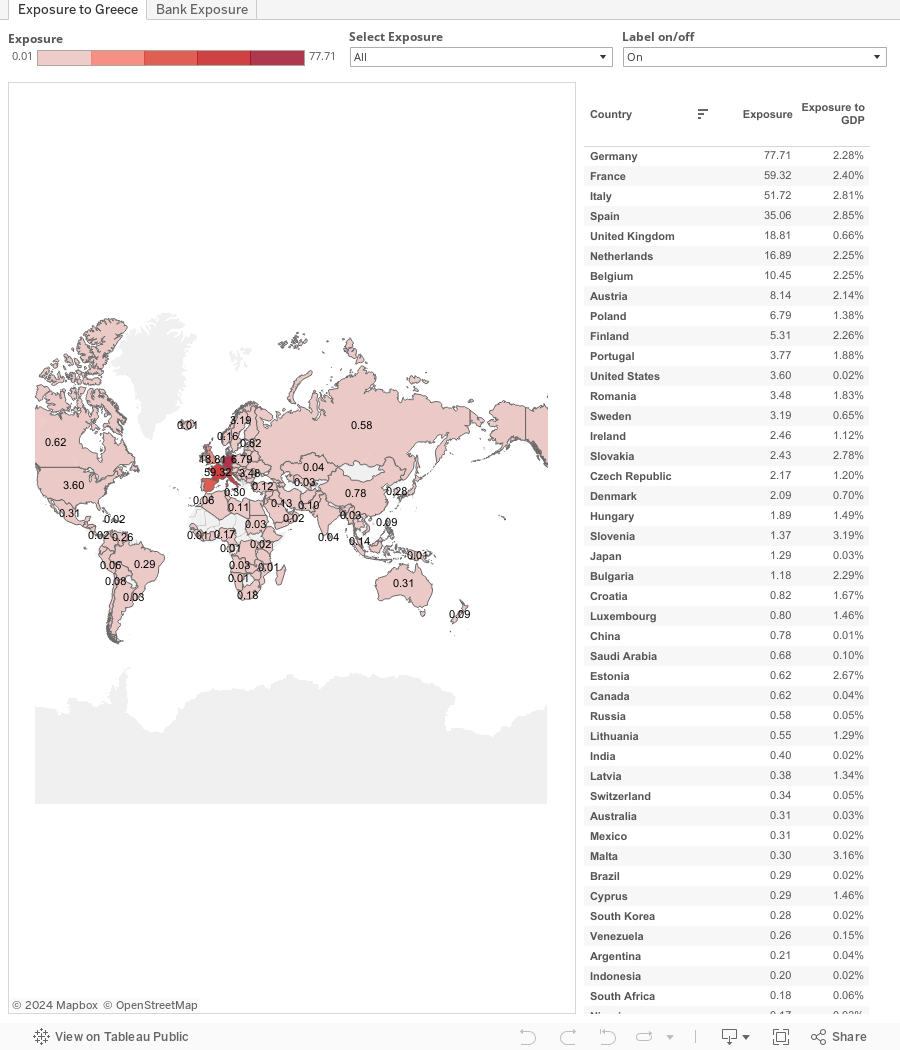

Who is hurt the most if Greece defaults?

The first tab shows the exposure of all countries in the world to Greek sovereign debt. The vast majority of Greek sovereign debt is held by the EFSF (€131 bn.), IMF (€21 bn.) and bilateral loans through the Greek Loan Facility (€ 53 bn.). For the EFSF and the bilateral loans, exposure of the different countries is calculated based on their contribution to these programs. For the IMF exposure is calculated based on IMF Members’ Quotas. Furthermore the ECB and all the national central banks hold Greek Bonds (€27 bn.) for which exposure of the different countries is calculated based on the ECB capital key.

Also included in this visualization is the TARGET2 exposure of Eurozone countries to Greece. TARGET 2 is the interbank payment system for cross-border transfers throughout the European Union. This system facilitates payments between Eurozone national central banks without the need for a direct transfer of assets. This enables fast transfers between Eurozone countries however it also creates liabilities between countries. The problem with these TARGET2 liabilities is that should a nation drop out of the Eurozone, these liabilities may not be met. In this case the ECB might have to take a loss which has to be covered by the remaining Eurozone countries. Currently Greece has a TARGET2 liability. This liability is divided over the Eurozone countries according to the ECB capital key.

Non-sovereign exposures are excluded from this visualization.

The second tab shows the exposure of banks to Greek debt through time. The data is retrieved from the bank of international settlements. One can clearly see that banks have decreased their exposure through time.

Amounts are in billion Euro’s.